This is not the first time I'm covering the topic of Keynesianism - as a matter of fact, this may very well be something like the 100th post I've written on the topic. This post however is a little bit different: Instead of just writing about keynesianism, I'm going to make a graphical presentation of the keynesian failure.

Keynesianism, in the most simple words, says that governments should run budget surpluses during booms, and then spend the saved money during recessions. Recessions, keynesians claim, is caused by a fall in total demand - basically, people refuse to spend money, which causes unemployment and a fall in output. Therefore, the government needs to step in and spend more money to compensate for the fall in consumer spending. Yes, the government may have to take on debt during a recession in order to do this, but it's okay - once the economy turns around, tax revenue will go up and the state will be able to afford to pay back the debt it took on during the recession.

One big problem with keynesianism, which I've talked about before, is the failure of governments to apply keynesian policies consistently: It's very easy to spend during recessions; but it's tougher to save during booms. Once a government has had a deficit for a few years, deficits become the norm, and deficit spending becomes a habit. And we all know that bad habits die hard.

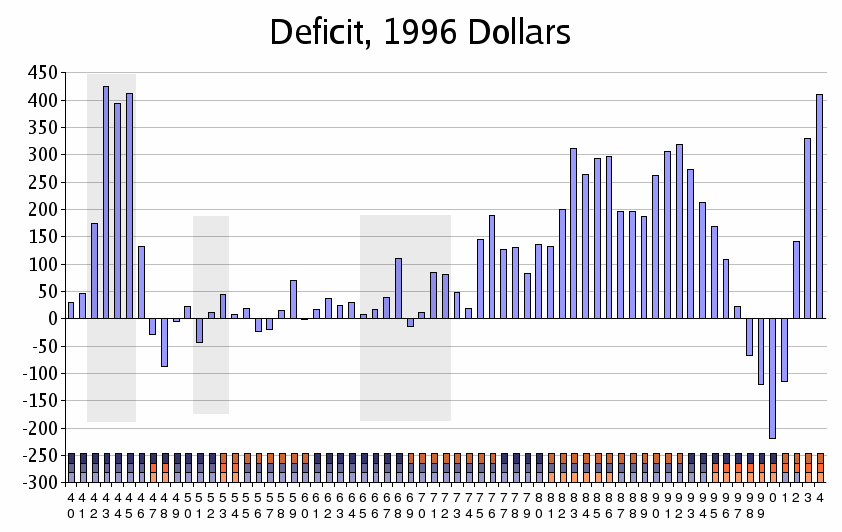

Have a look at these graphs if you don't believe me. Starting with the US deficit and growth of GDP:

Can you spot the problem? The US economy has been growing for most the time during the past 50 years, yet the budget hasn't been balanced for more than a few years since the 1960's. Yet, if keynesian policies had been followed strictly, the budget should have been balanced (or rather, in surplus) during all those years with positive growth.

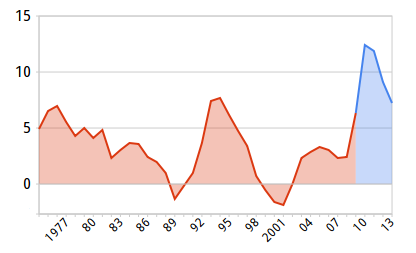

The trend is similar in Europe. Starting with the UK:

It's the same thing all over again: Growth is positive for all but three years (the yellow and blue areas are predictions made at the time), but the budget is unbalanced for all but 3-4 years.

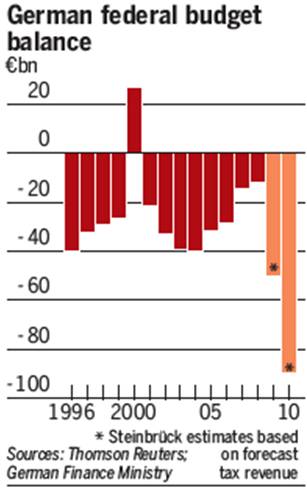

Next: Germany. Notice any familiar patterns?

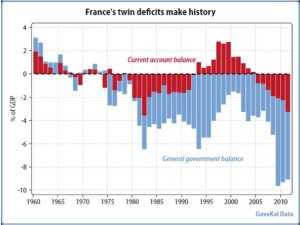

It's not looking good for France either (first graph shows annual growth, second shows deficit):

Basically, for those of you who find the graphs hard to read: France's economy has been growing since 1990 with only 3 years with negative growth, yet the french haven't balanced the budget since 1974!

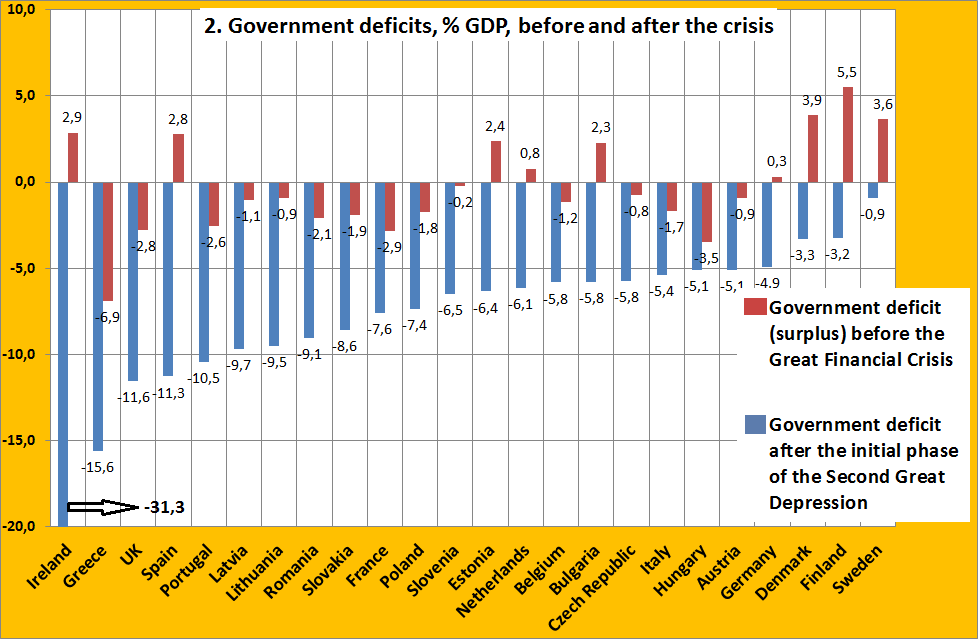

And, just to nail the coffin, here is a graph for all EU countries, comparing their deficits/surplus before and after the financial crisis:

For those of you who don't bother counting: Only 9 of these 24 countries ran surpluses prior to the financial crisis (adding insult to injury, two of these nine countries had very insignificant surpluses).

I freely admit that the data in the above graphs don't always cover the same time period, but I still think the case is pretty strong: Temporary deficit spending is and will always be a myth, a political utopia just as unreachable as the communist worker's paradise. Once you have a deficit, it's there to stay. This I believe is partly because it takes so long time to reduce a deficit, due to voters not being all that keen on tax hikes and cutbacks. By the time you've balanced the budget, another recession may already have arrived (economic downturns tend to happen at least every 10 years or so), and with the new recession comes new deficit spending.

You may wonder why I included stats for countries other than the US. The reason is simple: I'm trying to show that running deficits while the economy is booming isn't only an American probelm. Liberals like to claim that the only reason the US has suffered such permanent deficits is because of greedy Republicans refusing to pass tax hikes for the rich.

As you can see in the above graphs, that argument doesn't hold: There are no greedy Republicans in France, blocking tax hikes for high-income earners. Nor are there any greedy Republicans in Belgium, or Austria. And yet these countries ran deficits during booms.

Liberals at this point will probably suggest that keynesianism isn't to blame for this; after all, sure keynesianism only recently got a revival as an economic ideology? Keynesianism can't be blamed for deficits that occurred decades ago. But Keynesianism was never dead as a political ideology - true, Keynes lost followers among economic researchers when stagflation began in the 1970's (something that wasn't supposed to be possible according to Keynes), but unfortunately economic researchers don't dictate economic policy. Keynes still had plenty of followers among politicians; for them, it was as if the stagflation never happened. Keynesianism was just too valuable for politicians to give up; it gave them the perfect excuse to spend like there was no tomorrow. No pesky, stubborn facts and no annoying dismal scientist was going to take that excuse away from them!

The keynesian revival has occurred strictly among economists in academia, where keynesian theory has gained followers in recent years - the politicians however were keynesians all along, so no change there.

I wrote in an earlier post that it's very hard not only for individuals, but for governments as well, to break bad habits. The above graphs prove this beyond doubt. Quod Erat Demonstrandum.

Thanks for reading.

1 comment:

Great post, thanks. Never really understood keynesian economics quite like this before. I think my life is a microcosm of overcoming keynesianism. Btw, here's a great video on obama and keynesianism if you haven't seen it yet. http://www.youtube.com/watch?v=gBrHkxqNT7s

Post a Comment